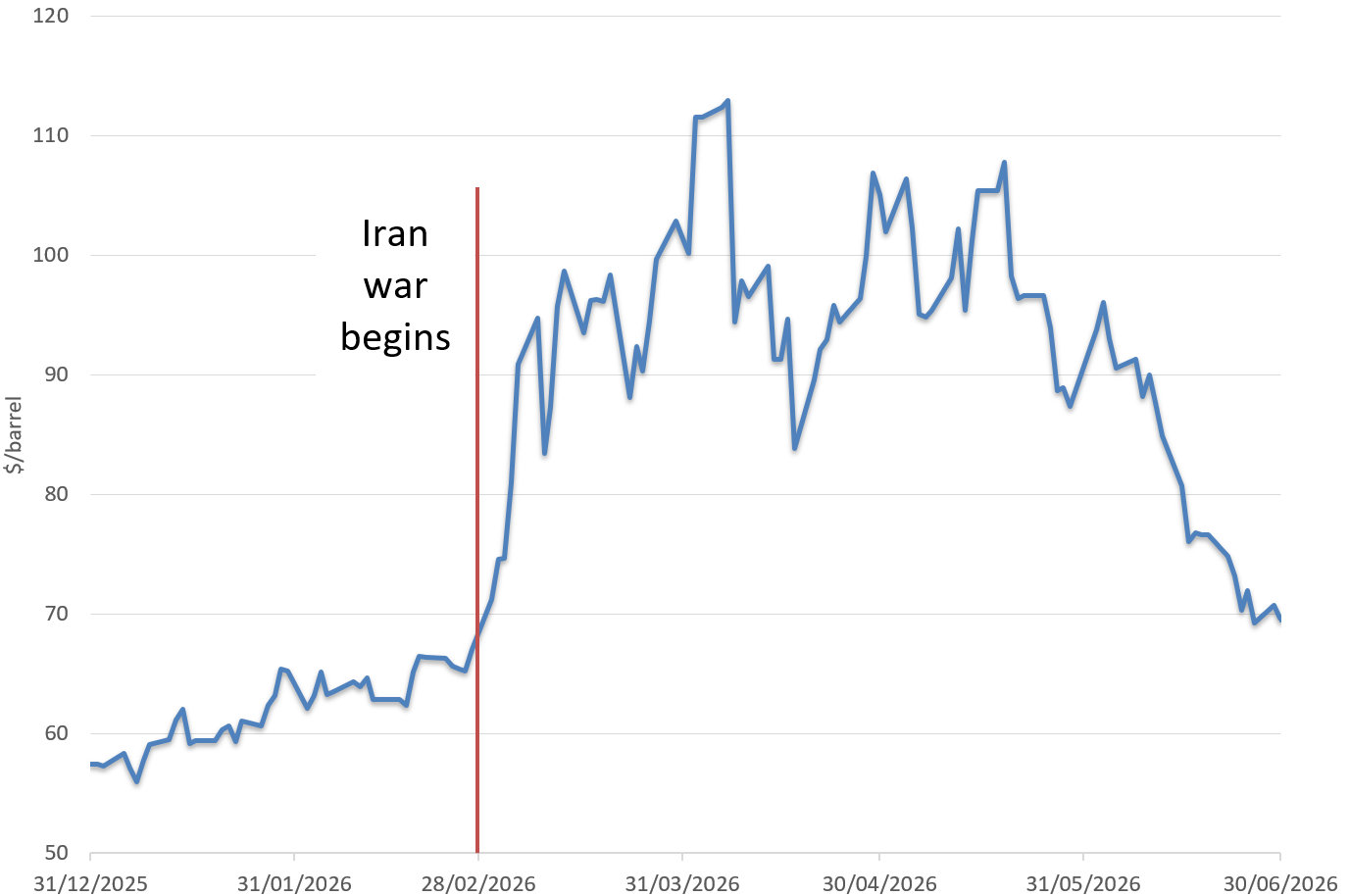

The issues that dominated markets in May continued into June, with the war in Iran remaining the key theme. Despite ongoing reservations about the scope of the memorandum of understanding (MOU) signed by the US and Iran, the interim deal initially helped oil prices move back towards pre-war levels after the Strait of Hormuz was reopened. That was an important development, given the impact higher energy prices have on inflation.

The past few weeks have been a reminder of how fragile this process is likely to be, with periods of calm punctuated by bursts of hostility. Most recently, the MOU was put at risk with both sides accusing the other of violating the ceasefire before another agreement to pause attacks and resume talks was reached. The two rivals have around 60 days to turn this framework into something more permanent and a lot can happen in that time.

The one thing that should help to secure a more permanent peace is the domestic political backdrop in the US. Donald Trump is heading into the midterms with growing scrutiny over the cost of the conflict, alongside some clear tensions within his own party, including about the terms of the MOU, which has widely been interpreted as a capitulation to a defenceless aggressor. It has to be hoped that this political pressure helps to desensitise Trump’s itchy trigger finger.

For markets, the key point is that oil prices have fallen rapidly and while they’ve experienced more volatility as tensions oscillated, as far as traders are concerned, the war is seemingly in the rear-view mirror. Of course, that doesn’t mean everything has normalised overnight. Even with shipping routes reopening, it takes time for flows to recover and there is a lot of work to do before the disruption caused by the war is unwound.

Recent data has already shown some improvement in headline inflation, but, as we highlighted last month, not all of that improvement should be taken at face value. Some of the better numbers have been helped by technical factors and the way previous price moves feed through the data, rather than by a clear easing in the pressures households actually feel.

That makes the near-term outlook hard to anticipate. If energy prices remain contained, inflation should continue to drift lower. If they rise again, particularly alongside higher food and transport costs, the progress made so far could quickly unwind.

Oil price recovery

Source: FactSet, year to the end of June 2026

The big central banks are responding to that uncertainty largely by doing very little. The Bank of England (BoE) and the Federal Reserve (Fed) both declined to follow in the footsteps of the European Central Bank, with each choosing to hold interest rates at their recent meetings. All three banks expect inflation to be higher than previously forecast this year, but there is still a live question over what further rate rises would actually achieve if much of the pressure is coming from a temporary spike in oil prices. Higher interest rates can reduce demand, but they won’t produce more oil or guarantee that shipping routes remain open.

The BoE had two members vote for a rise while in the US, all 12 members of the Fed’s rate-setting committee voted to leave rates unchanged, the first time that has happened for 12 months. That unanimity is useful for new chair Kevin Warsh. Trump has been vocal in his expectation that borrowing costs should be moving lower and he was highly critical of Warsh’s predecessor, but the inflation picture hasn’t given the Fed much room to act.

That is a meaningful change in tone. Markets had become fairly comfortable earlier in the year with the idea that interest rates would start coming down in a relatively orderly way. That still might happen, but the path looks less certain now. While this does not necessarily mean that rates need to rise, it does suggest that the “higher for longer” environment has not disappeared. Borrowing costs may stay elevated for longer than markets had hoped earlier in the year.

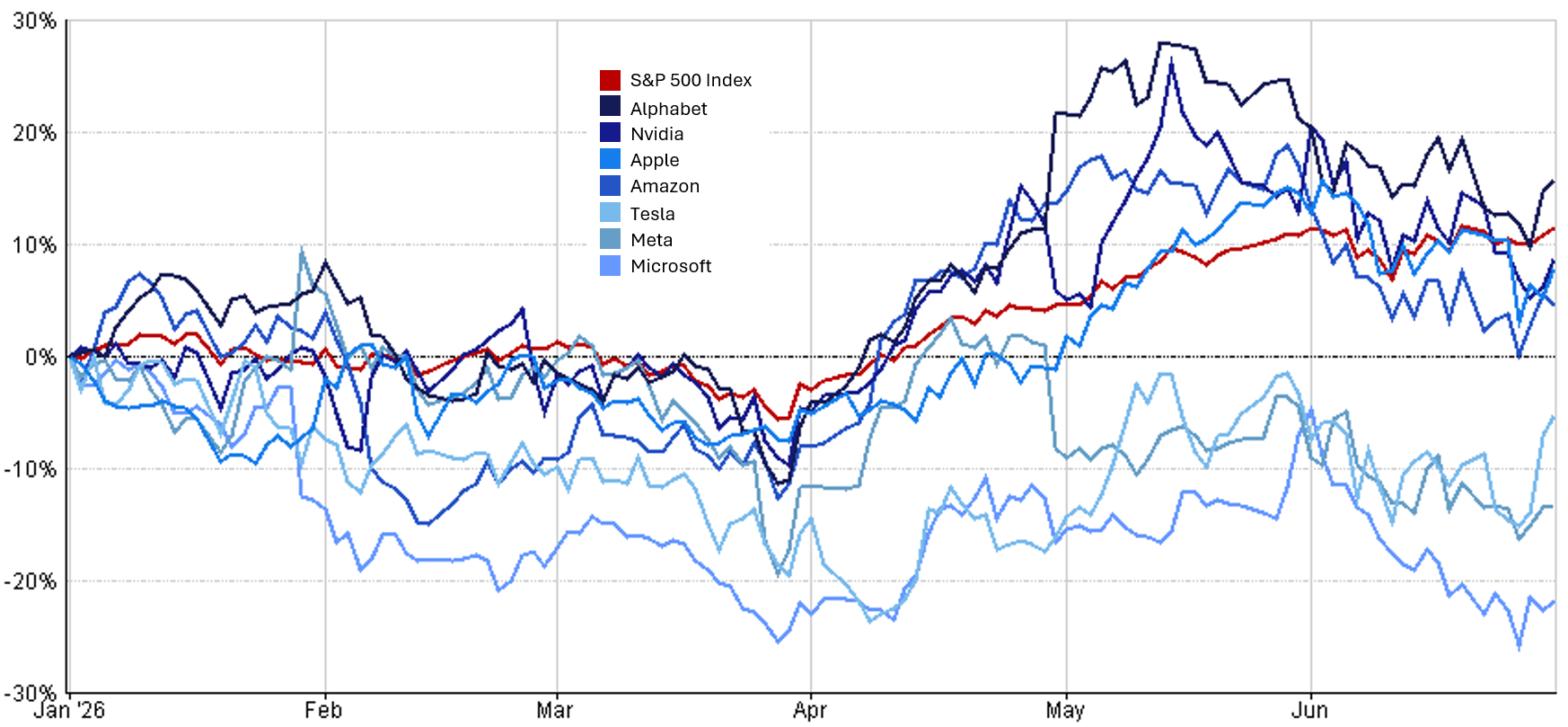

Against that backdrop, equity markets have held up relatively well. The main US index remains close to its record high point, although progress has stalled somewhat over the last month. Weaker returns from the Magnificent 7 tech names have been a headwind, and while there have been periods where chipmakers have picked up the slack, it’s a further sign of a shift in the AI trade. Earlier in the year, investors seemed happy to buy almost anything connected to the theme. More recently, the market has been more selective.

There are a few possible explanations for that. It could be a rotation into the firms supplying the chips away from those using them, concerns about interest rates, or ongoing concerns about the level of investment and borrowing required to support the AI build-out. Apple shares, for example, recently experienced its second worst ever one-day fall after announcing a 20% price increase on its laptops, caused by shortages in memory chips.

Another element giving investors pause is the SpaceX initial public offering (IPO). Elon Musk’s company, best known for its rockets and satellite network but now also heavily involved in AI, raised a record-breaking $75bn in an IPO that was oversubscribed three times. The shares initially rose by close to 70% before giving back a meaningful part of those gains, although they remain well above the IPO price and the company already sits among the largest businesses in the US.

Alongside the expected listings of OpenAI, the company behind ChatGPT, and Anthropic, one of its main rivals, later this year it highlights the scale of capital still being drawn towards AI and the surrounding ecosystem. Index providers have jumped on the bandwagon by changing their rules to speed up inclusion for these businesses. This means they can quickly become part of some passive funds which is likely to add to demand from active investors and result in money being pulled away from existing holdings as the new entrants come to market.

The Not So Magnificent Seven?

Source: Financial Express Analytics, year to the end of June 2026

None of this means the AI theme is wrong. The technology may well prove as important as its advocates suggest. The issue is more about expectations. When a lot of future success is already reflected in share prices, companies need to keep delivering against very high assumptions. Strong results are no longer always enough if investors were already expecting them.

This links back to the point made last month around concentration. A relatively small number of companies have driven a large share of market performance, particularly in the US, for much of the last few years. That can support returns when sentiment is positive, but it also leaves less room for error. If the market starts to question how quickly AI spending turns into profit, the effect could be felt across a wide range of businesses that are increasingly connected to the same theme.

There is also a broader economic point here. First quarter US GDP was revised down slightly to 1.6%, which is still robust, but more than half of that number is estimated to have come from the rollout of AI infrastructure. That highlights just how much now rests on the success of this technology, even outside the stock market.

As with the idea of a K-shaped economy, where the richest people are thriving while many others are barely surviving, there has been a similar split in markets this year. The headline index has performed well, but look beneath the surface and the picture is less even. Consumer-facing sectors have been under more pressure, while companies linked to AI have carried a far greater share of the return, at least until the last month. Bond markets have been telling a more cautious story. Yields have remained elevated as investors price in the risk that inflation proves more persistent and interest rates stay higher for longer. History suggests that these two signals do not usually sit well together.

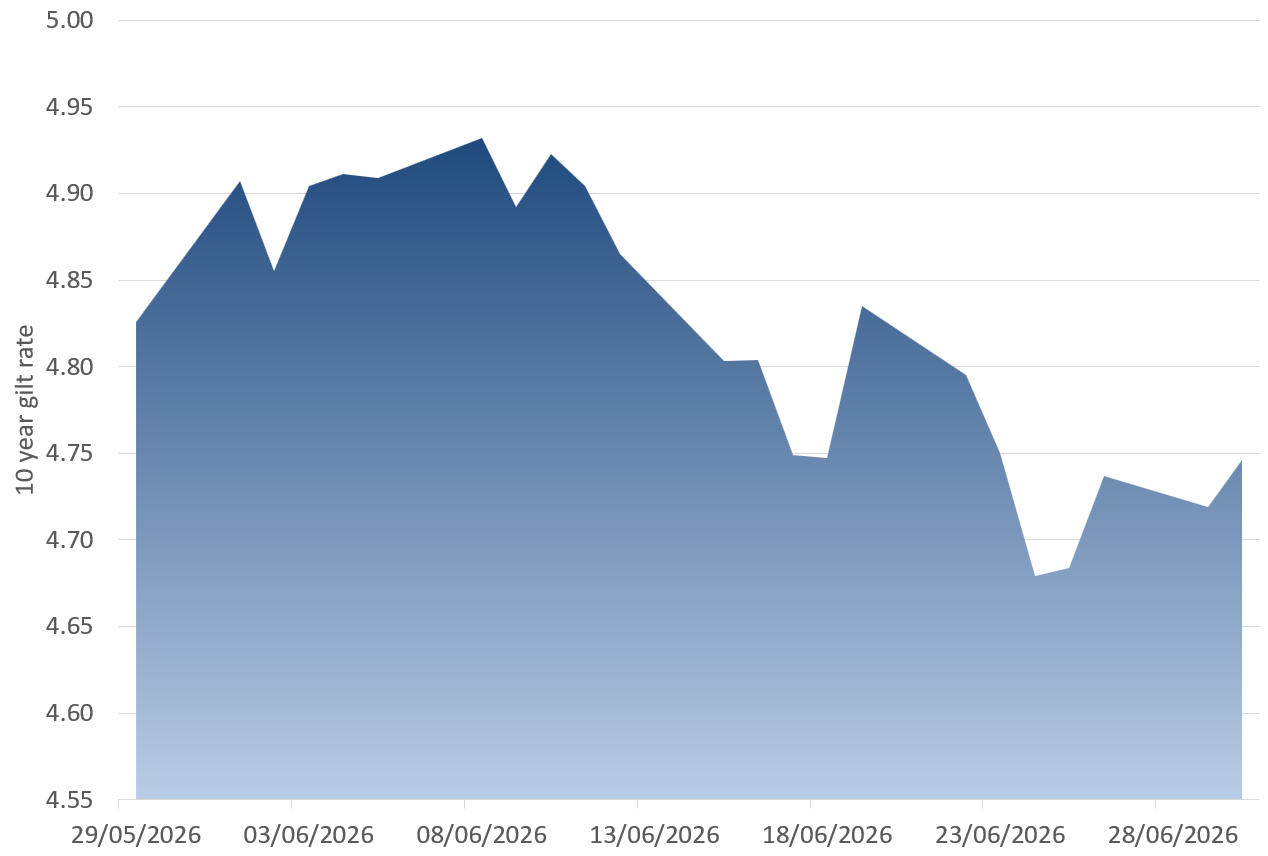

In the UK, gilt yields moved higher at times during the month but the reaction to political developments was more measured than might have been expected. The revolving door at Number 10 attracted attention, and Keir Starmer’s resignation opened the door for Andy Burnham to take the reins at the top of the Labour party. That led to speculation about whether we might see more spending, but the immediate market reaction was muted. Gilt yields moved slightly higher before retreating, while sterling was steady. Burnham has been keen to assert that he does not intend to drift from the fiscal rules set out by Rachel Reeves but the market will reserve judgement until his pick for chancellor is announced.

UK gilt yields

Source: FactSet, June 2026

To recap, the MOU between the US and Iran has reduced some of the immediate pressure in energy markets, but the process remains fragile. Central banks are waiting for clearer evidence before making their next move. Equity markets remain resilient, but the leadership is narrow and still heavily tied to AI.

In these conditions, our focus remains on balance rather than trying to anticipate a single outcome. Markets have shown an ability to absorb a wide range of news, but that does not remove the need for discipline. With inflation still uncertain and expectations high in parts of the equity market, the aim is to keep portfolios robust across a range of scenarios rather than making large short-term adjustments in response to each new headline.

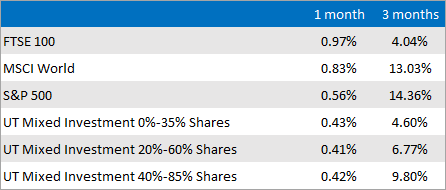

Market and sector summary to the end of June 2026

Source: Financial Express Analytics.

Past performance is not a guide to future performance, nor a reliable indicator of future results or performance.