Thank you to everyone who has already responded to the latest review of the IMS portfolios which was sent out last month. We’ve had an excellent response so far, but if you have not yet had an opportunity to send us your acceptance, we would be grateful if you could so that we can make sure your investments are in the current fund selection. You can respond to this message if you would like another copy of the review to be sent out.

The main theme of May continued to be the ongoing fallout from America’s war with Iran, with the path for inflation and interest rates far less straightforward than it appeared earlier in the year. The key issue from an investment perspective is the impact that the war has had on global energy prices and, in turn, the cost of food and other essentials.

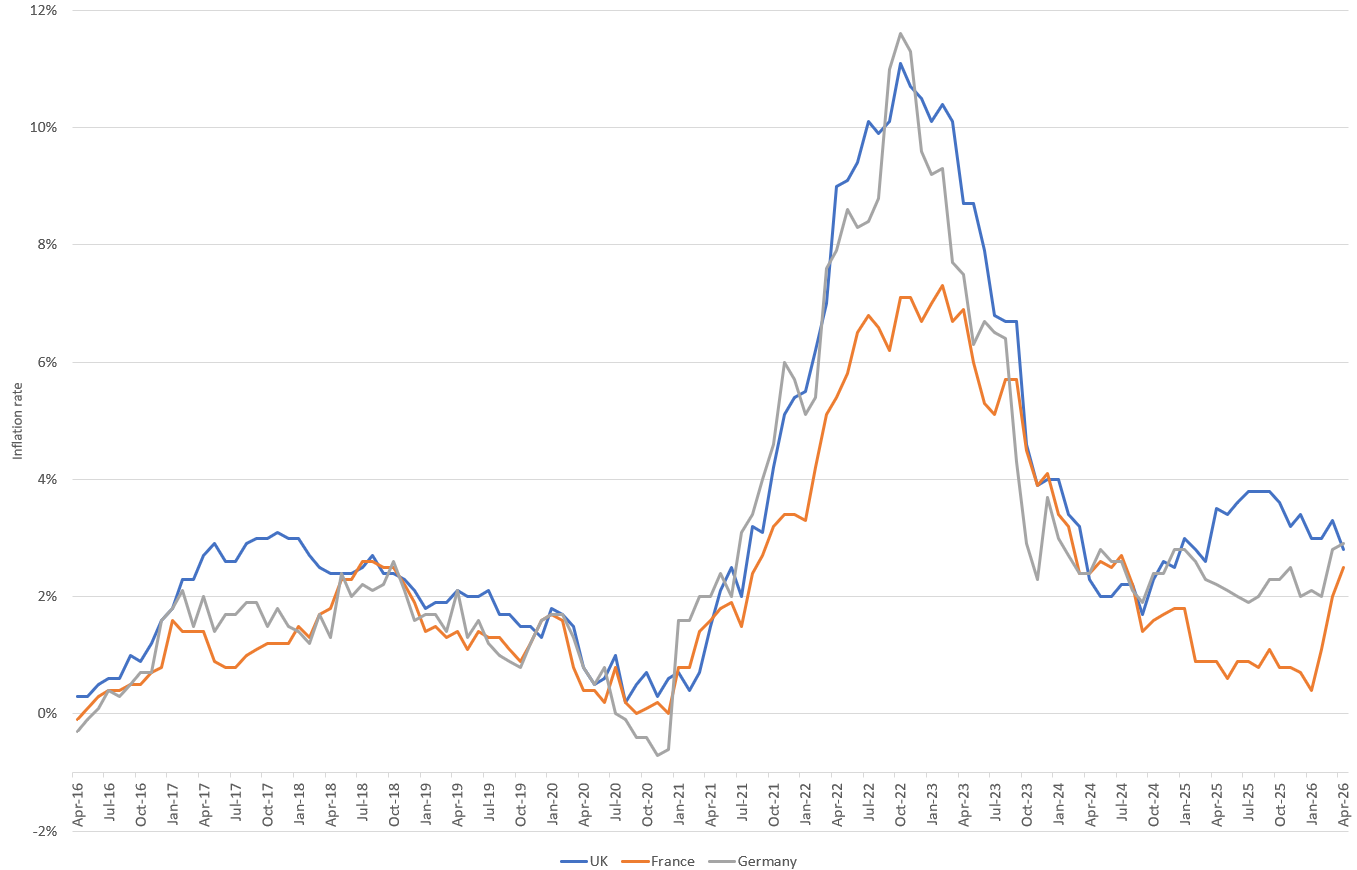

Recent data has shown some improvement in headline inflation, but much of that has been driven by technical factors rather than an actual reduction in underlying pressures. In the UK, for example, we saw the rate fall to 2.8% for the 12 months to the end of April, a big fall from the 3.3% reading the month before. However, the decline was heavily influenced by changes to the energy price cap, which reflects historic pricing rather than current events, and the prevailing view is that this will prove temporary.

A brief respite?

Source: Office for National Statistics

Looking beyond that near-term relief, the outlook is complicated by the ongoing impact of higher energy prices and geopolitical developments. This makes it much harder to take a confident view on the trajectory for inflation from here, particularly as some of the apparent improvement in the data is likely to unwind as more recent price increases filter through. Central banks are increasingly focused on the risk that these pressures prove more persistent over time.

That uncertainty is feeding directly into predictions for interest rates. Where markets had previously been comfortable with a steady path towards rate cuts, the picture has become less clear, with policymakers adopting a more cautious “wait and see” approach. The key question is now how sustained any inflationary pressures prove to be.

Taken together, this points towards an environment that is better characterised as “higher for longer” rather than one where rates are about to fall quickly. That does not necessarily imply further increases to interest rates, although that is not off the cards, but it does mean that borrowing costs are likely to remain elevated relative to what had been assumed earlier in the year.

Against that backdrop, markets have remained relatively resilient, but there is an increasing sense that different asset classes are telling conflicting stories. Equity markets, particularly in the US, have performed well, supported by strong earnings and ongoing enthusiasm around areas such as artificial intelligence. In fact, the recent earnings season, where companies report on their revenues each quarter, was one of the best in the last 20 years. 84% of companies in the main US index produced numbers that were ahead of estimates. At the same time, bond markets have taken a more cautious view, with yields rising as investors price in the risk of more persistent inflation and tighter financial conditions.

US resurgence

Source: Financial Express Analytics, 28/04/2026-28/05/2026

Those two signals generally do not sit comfortably together. Bond markets are effectively pointing towards a more restrictive environment, while equity markets have continued to behave as if everything is perfect. Periods like this can persist, but they tend to increase the likelihood of some form of adjustment if one side of the market proves to be too optimistic.

In the UK, this dynamic has been reflected in a sharp move higher in gilt yields. While some of this reflects global factors, local dynamics have also played a role, particularly given the UK’s sensitivity to energy prices and the resulting uncertainty around the inflation outlook. This has reinforced the case for a more diversified approach to fixed income rather than a concentrated exposure to any one market.

Valuations remain an important part of that discussion. While there has been some easing in parts of the equity market earlier in the year, overall levels are still not obviously cheap, and expectations are still elevated. This leaves limited margin for error and makes markets more sensitive to changes in the outlook, whether that comes from interest rates or corporate earnings.

There has also been a subtle evolution in market behaviour over recent months. Earlier in the year, investor enthusiasm around certain areas of the technology sector was largely unquestioned, but there are signs that markets are becoming more focused on the relationship between valuations and actual delivery.

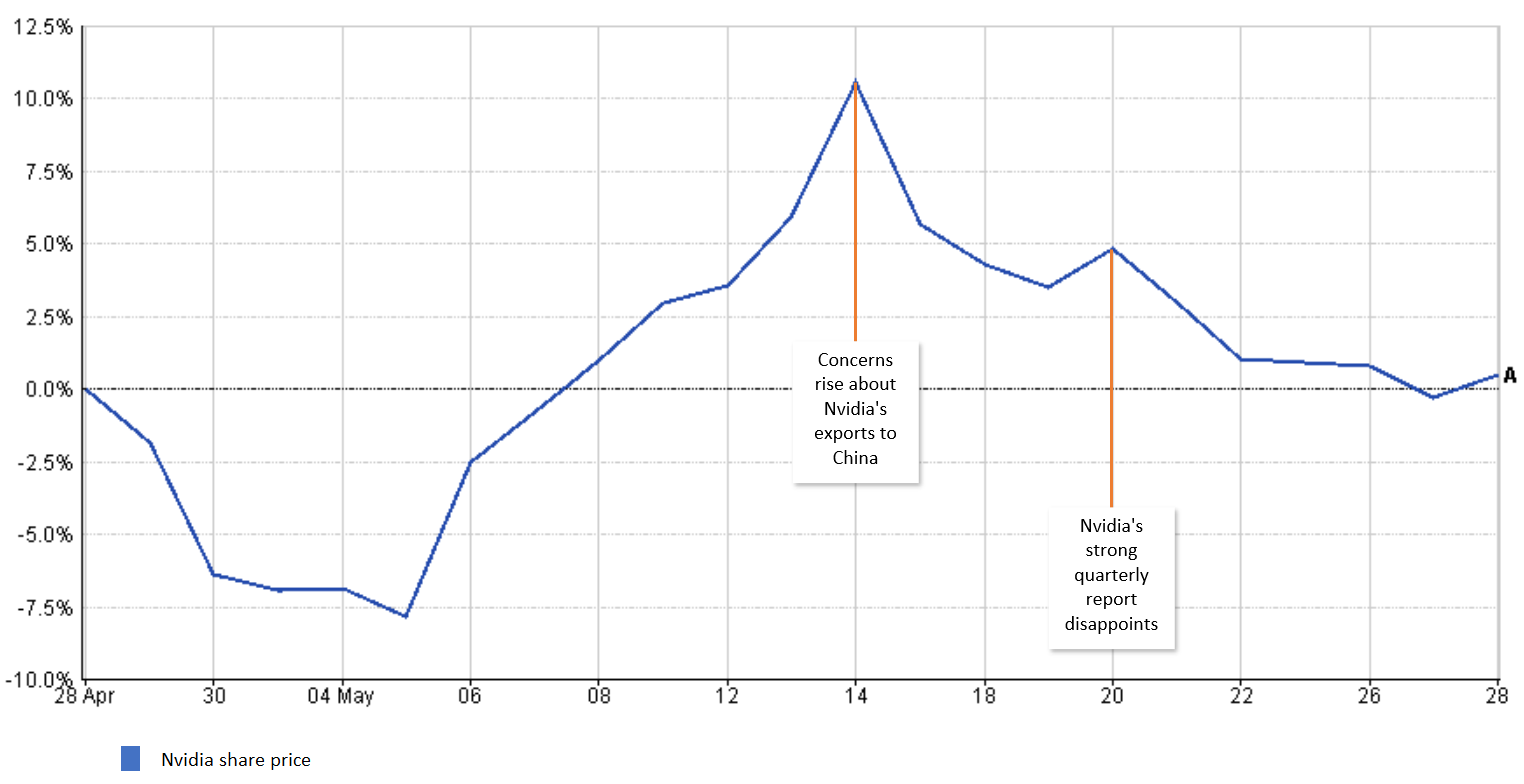

That shift in behaviour was evident in the market reaction to Nvidia’s latest results. The company once again delivered an exceptionally strong set of numbers, with revenue and earnings comfortably ahead of forecast and no let-up in demand for artificial intelligence infrastructure. Despite this, the response was muted, with the share price moving lower in the immediate aftermath. Their shares are down 10% from their peak last month.

Share price struggles at the world’s largest company

Source: Financial Express Analytics, 28/04/2026-28/05/2026

This reflects how much optimism is already built into markets, with investors focused less on whether companies can beat forecasts and more on whether that growth can be sustained. Strong results are no longer enough on their own when valuations and positioning are already elevated, and shareholders are increasingly looking for evidence that current levels of investment, especially in areas such as AI, can translate into durable returns over time.

Linked to that is the issue of concentration. Market performance has continued to be driven by a relatively small number of companies and sectors, particularly within the US. While this can support performance when conditions are favourable, it can also increase fragility if sentiment begins to shift, as narrow leadership tends to leave less room for error.

This is exacerbated by the level of interconnection between lots of these firms, where many are both suppliers and customers to one another, recycling capital across the same ecosystem. This can amplify growth when conditions are favourable, but also means any slowdown can spread more quickly across the market.

In these types of conditions, the case for diversification and a focus on valuation becomes ever more relevant. Our objective is not to anticipate a single outcome or to make large short-term adjustments, but to ensure that portfolios remain robust across a range of potential scenarios.

The underlying picture remains uncertain and no clear resolution appears to be on the horizon. Inflation is likely to remain a headwind, interest rate policy is finely balanced, and market behaviour continues to reflect that tension. With this backdrop, the focus therefore remains on maintaining balance rather than making significant calls as we navigate what is still a complex environment.

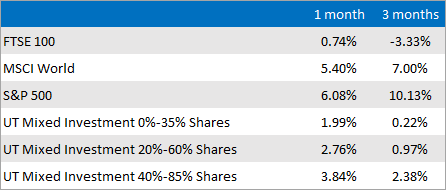

Market and sector summary to the end of May 2026

Source: Financial Express Analytics.

Past performance is not a guide to future performance, nor a reliable indicator of future results or performance.