March was dominated by developments in the Middle East as the conflict between the US, Israel and Iran continued to unfold. Events moved quickly as the month progressed, often with limited clarity around the political end game. While the humanitarian impact remains a serious concern, from an investment perspective the market implications centred on risks to energy supplies, shipping routes and knock-on effects on inflation.

With the conflict reshaping the backdrop for policymakers and investors, it is worth taking stock of how March unfolded and what it has meant for markets. This remains a rapidly evolving situation and the commentary below should be read with that in mind.

The most prominent source of uncertainty came from the competing narratives emerging from Washington and Tehran. President Trump vacillated between insisting that the US would continue its attacks and suggesting that productive peace talks were under way, even claiming that high value gifts had been offered by the Iranian leadership. However, senior Iranian officials have denied that any discussions had taken place and described the claims as fake news. This inconsistency did little to calm markets, particularly as Iran continued to launch missile and drone attacks across Israel and Gulf states.

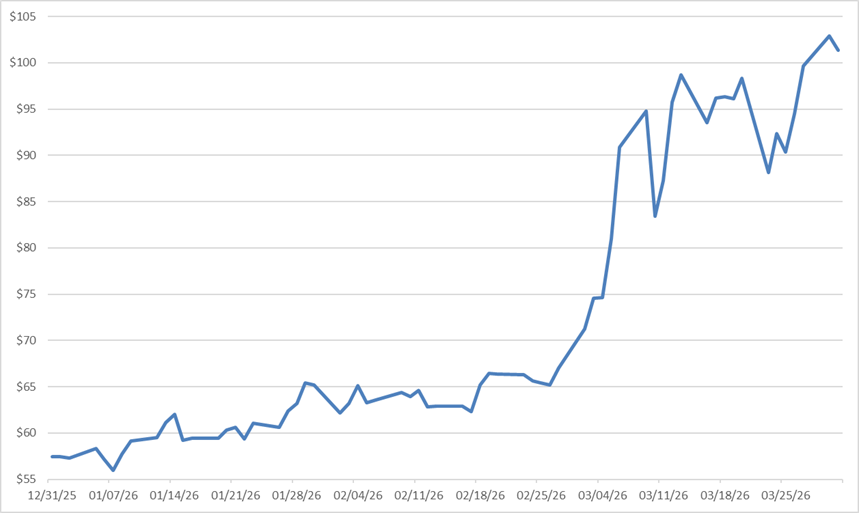

The conflict rapidly became an economic story as much as a geopolitical one. Shipping through the Strait of Hormuz slowed to just a handful of transits a day, with tanker attacks, threats to mine the Persian Gulf and strikes on key oil and liquefied natural gas infrastructure limiting the movement of goods. Maritime insurance became extremely expensive or unavailable in several cases. These pressures repeatedly pushed oil prices above $100 a barrel and sent global gas prices higher, feeding straight into inflation expectations across major economies.

Oil prices high and volatile

Source: Factset, 01/01/2026-31/03/2026

Central banks correspondingly became more cautious around their plans for reducing interest rates. The US Federal Reserve (Fed), European Central Bank and Bank of England all left rates unchanged at their latest meetings, but their language signalled a clear shift in focus. UK gilt yields rose to their highest levels since 2008 as markets reduced expectations for near-term cuts. Fed Chair Jerome Powell acknowledged that rate hikes had been discussed, an unwelcome development for those expecting a smoother path towards easing over the rest of the year.

Despite all of the understandable focus on this situation, it is worth remembering that the recent volatility has not been as severe as headlines might suggest. While the UK's main index has fallen around 6% since the start of hostilities, this is smaller than the 11% drop seen during last April’s tariff turmoil, which was fully reversed within a month. The current episode has been sharper in places, but overall the impact has been more gradual and less extreme.

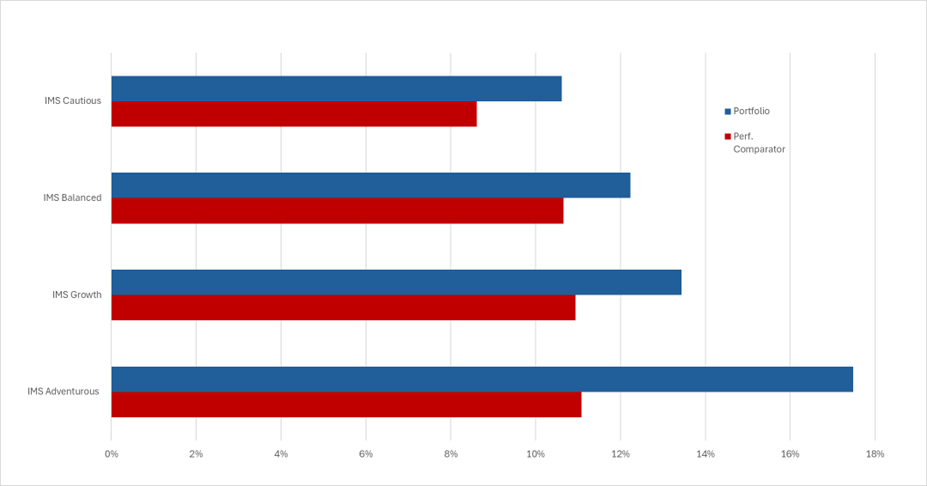

Equity market leadership also broadened during March. While the Magnificent Seven continued to lose momentum, around half of US and other developed market stocks outperformed their respective index averages, something rarely seen when the big tech firms were dominating returns. This is a much healthier environment for diversified portfolios like ours. Despite the noise, the main IMS Capital Accumulation portfolios have retained strong performance over the last twelve months, on both an absolute and relative basis.

IMS 12-month performance

Source: Financial Express Analytics, 31/03/2025-31/03/2026

Away from events in the Middle East, private credit also returned to focus during the month. Private credit refers to non-bank lending where private capital firms provide direct loans to companies, typically bypassing public markets and traditional financial institutions. The loans that they issue are not themselves liquid, so the funds in which they sit are often structured as semi-liquid, allowing investors to withdraw capital only at specified intervals and within set limits.

The failures of Tricolor and First Brands last year, both largely seen as fraud related, had already prompted questions around transparency and valuations. These concerns intensified when a company called Blue Owl blocked withdrawals on some of their retail focused funds. BlackRock then capped withdrawals after elevated redemption requests, while Blackstone avoided doing the same only because its own employees contributed significant capital to meet outflows.

Other firms have since taken similar steps and, were it not for events in the Middle East, it seems likely this might have been a more widely covered theme. Although the issue is not about a sudden deterioration in credit quality, it represents a reappraisal of how private market structures behave when conditions tighten.

As March drew to a close, the interaction between geopolitics and inflation expectations remained the key theme. Even if energy prices moderate, supply chain effects in areas such as fertiliser and shipping tend to feed through with a lag. Energy costs can fall quickly if conditions improve, although continued attacks on fuel facilities do increase the risk of longer-term impacts, but food costs rarely do. This is why central banks remain wary and why markets have adjusted to the likelihood that interest rates may stay higher for longer.

Our portfolios remain positioned with diversification in mind and recent events have not materially altered our longer‑term outlook. We have no direct exposure to the areas under the most scrutiny in private markets, and our allocations to energy sensitive and defensive sectors helped stability during the month. Periods like this have historically tended to favour patience over attempts to respond to short‑term market moves. Should geopolitical tensions ease, some of the recent risk premium may unwind, but for now markets continue to be shaped by headlines and rhetoric.

Market and sector summary to the end of March 2026

Source: Financial Express Analytics.

Past performance is not a guide to future performance, nor a reliable indicator of future results or performance.