Thank you to everyone who has already responded to the latest review of the IMS portfolios which was sent out last month. We’ve had an excellent response so far, but if you have not yet had an opportunity to send us your acceptance, we would be grateful if you could so that we can make sure your investments are in the latest fund selection. You can respond to this message if you would like another copy of the review to be sent out.

The past few weeks have been marked by a somewhat strange dichotomy in markets. On one hand, high-flying US technology stocks have hit a wobble as investors began to demand tangible returns on their massive investments in artificial intelligence (AI). On the other hand, a wave of volatility has struck a range of service-sector companies as markets rapidly price in the risk that new AI tools could challenge their business models.

For much of the past few years, investors were willing to overlook the sky-high valuations at the biggest Silicon Valley firms as long as those companies told a compelling growth story, primarily focused on breakthroughs in AI. That patience has started to run thin as these firms continue to burn through huge sums to pay for these developments. The question has shifted from simply “how big could the AI opportunity be?” to “when will we actually see profits from all this spending?”.

This change in mood has triggered a broad pullback in mega-cap tech shares with several of America’s largest tech names struggling year to date. Importantly, it’s not due to any single earnings miss or company-specific issue. Rather, investors appear to be reassessing the entire AI investment narrative.

A core concern is that the cost of building AI infrastructure has exploded, and it remains unclear whether end-user demand will ramp up as quickly as investment. Each time a major tech firm announces ambitious new AI plans, they seem to outstrip the last round of forecasts, prompting markets to ask whether customer adoption can keep pace with this spending spree. So far, the answer is uncertain.

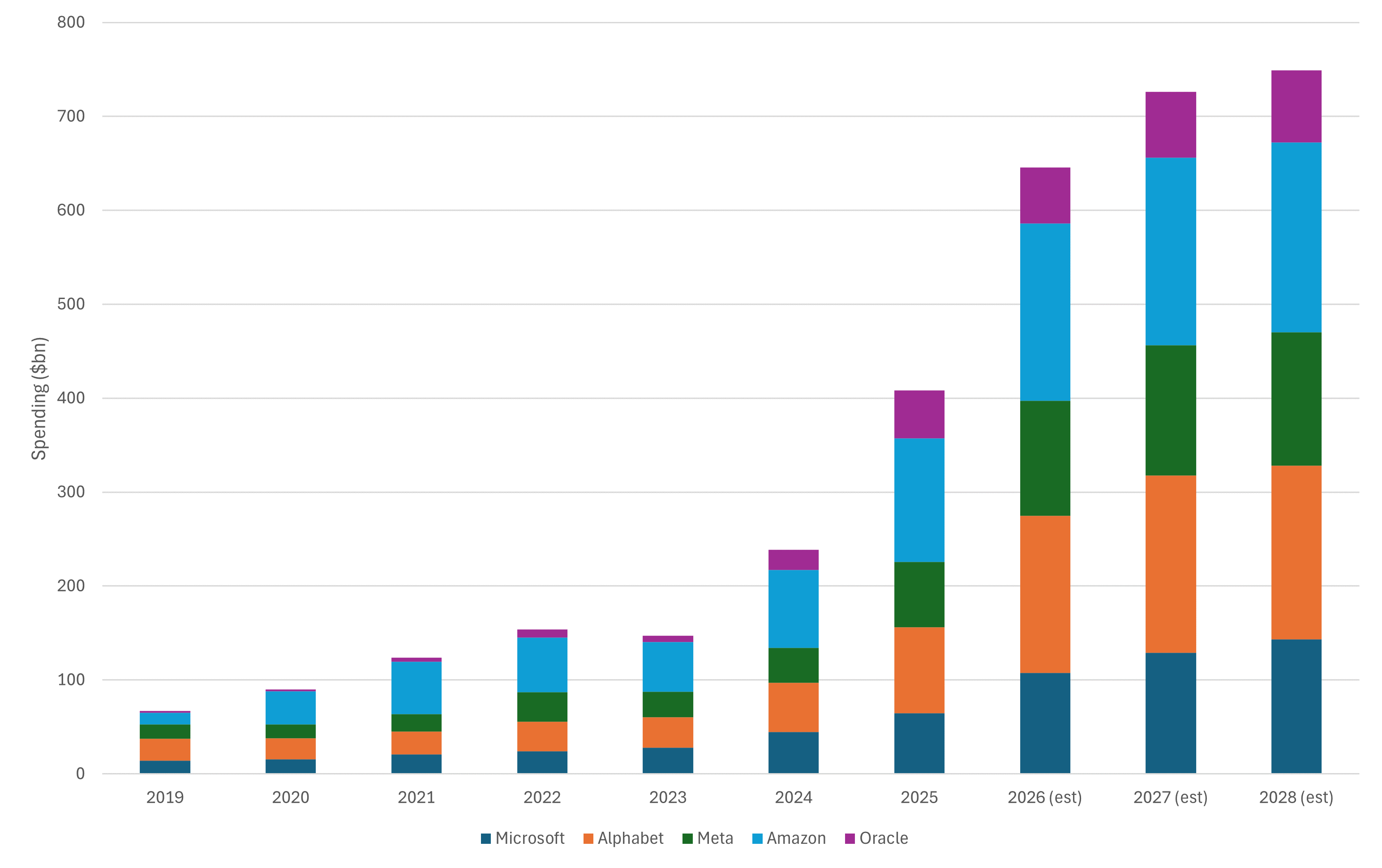

To put the scale in perspective, the so-called hyperscalers (Alphabet, Microsoft, Meta, Amazon and Oracle) are on track to spend roughly $650 billion this year on data centres and related AI infrastructure. This is comparable to the total economic output of countries like Singapore or Sweden and equal to the total value of all companies in major stock markets like Indonesia or Denmark.

Hyperscaler spending plans

Source: Factset

We’re also seeing a shift in how these expansions are being funded. There’s a trend towards borrowing to fund AI build-outs instead of relying solely on current profits. A striking example came from Alphabet (Google’s parent company), which recently issued a 100-year sterling bond which raised almost £1 billion. The issuance was oversubscribed nearly tenfold, showing that there are still investors willing to underwrite the ultra-long-term AI story, but paying for it through debt rather than earnings is a materially different proposition.

Another factor amplifying the tech sector’s gyrations is market concentration. A handful of mega-cap stocks have carried the market upward in recent years. That narrow leadership left indices vulnerable because when sentiment sours on that small group of very large names, the index-level impact is amplified. We’ve effectively moved from a phase where concentration boosted returns to one where concentration increases fragility. It seems like investors were unsure which firms would dominate the AI revolution so they “bet” on all of them. Now we’re arguably seeing a bit more common-sense return.

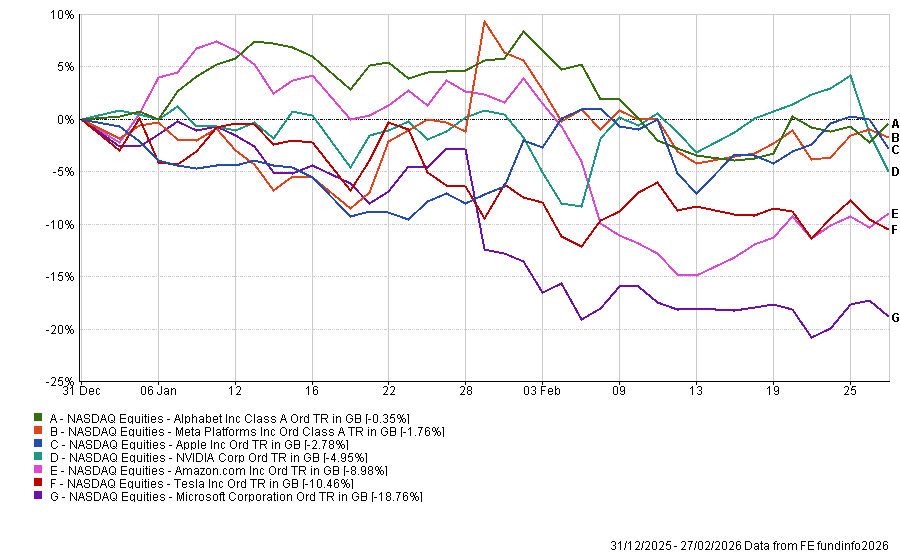

The Magnificent Seven?

Good companies and less-good companies had all been rising together. Now the tide is going out and could start to expose overpriced firms. The silver lining, from our perspective, is that the market’s reappraisal aligns well with how our portfolios were positioned. We had long been highlighting the risks of an overly concentrated market and the increasingly stretched valuations of the biggest tech names, and we maintained diversified exposure rather than chasing the ultra-expensive leaders. As a result, the recent tech stumble has benefited our portfolios on a relative basis.

Although our year-to-date returns are strong, we should be clear: we are not calling an official end to the AI theme. AI remains a powerful force with significant political and corporate backing. Everyone from industry CEOs to policymakers (up to and including Donald Trump) continues to push for ever-greater rollout of AI tools, given their importance to innovation and economic growth. In short, we fully expect this theme has more room to run, though perhaps with a bumpier road and a more discriminating market eye from here on out.

Despite the cool-down in Silicon Valley, the effects of AI are already being felt elsewhere in the market. Not so much through concrete changes in earnings (for now, at least), but through investors trying to account for future disruption.

A clear example emerged in the UK financial services and platform sector. In recent weeks, shares of several British wealth management, financial advice, and comparison platform firms tumbled after the launch of AI-driven adviser workflow tools in the US. Their business models didn’t disappear overnight, but the market started pricing in lower future earnings for companies which might be vulnerable to automation. Investors are looking at the rapid pace of improvement in AI and extrapolating that tools could soon handle tasks that were once the exclusive domain of skilled professionals.

The challenge, of course, is figuring out which firms are truly at risk and which fears might be overdone. Companies which were until recently seen as having dominant positions in the market have started to come under scrutiny. This explains why some share price swings have been so extreme. It’s not a measured, fundamentals-driven re-rating; it’s a rapid, fear-driven de-risking of any business perceived to be exposed to white-collar automation. Some caution is entirely rational as AI capabilities have genuinely leapt forward and will change certain industries. However, it’s also likely that the market is overshooting in places. Highly regulated, trust-based sectors are not going to be entirely disrupted by AI overnight.

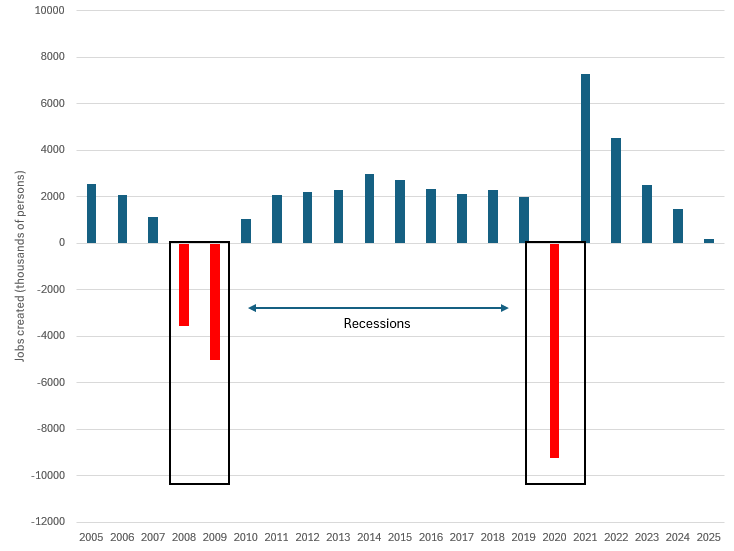

Another intriguing aspect is how the macro environment is interacting with these AI trends. The US economy, for instance, has given mixed signals. Headline growth has been relatively robust, but if you look at the details, the labour market is showing softness with fewer job vacancies, and workers are losing some bargaining power. In fact, 2025 saw the slowest year of US job creation (outside of recessions) in two decades.

US employment data

Source: Factset

One popular theory is that companies are “front-running” AI. Essentially, firms are already slowing hiring and redesigning workflows in anticipation of future productivity gains from AI. If true, we could be entering a phase where GDP growth holds up (thanks to efficiency gains) even as employment growth cools. This is more unusual than a standard slowdown and it could be a tricky situation for politicians to manage.

From an investment perspective, these challenges have triggered a notable rotation in markets. Money has been flowing out of the expensive big tech and at-risk service providers, and into areas seen as more insulated. Defensive sectors like healthcare and utilities have received a boost, as have traditional industries such as energy and industrials. Smaller companies have also begun outperforming their large-cap growth counterparts in recent months. This trend is another boost for our portfolios, which generally maintain broad diversification including meaningful mid- and small-cap exposure. It’s a refreshing change after a long stretch where a handful of large growth stocks seemed to overshadow everything else. A broader market leadership is healthier and it creates opportunities for value and quality-focused strategies to shine.

While technology and AI have dominated the narrative, towards the end of the month we had an interesting distraction with the news that the US Supreme Court had struck down President Trump’s “Liberation Day” tariffs. Markets initially welcomed this decision, however, celebrations were short-lived. In a characteristically bombastic response, President Trump announced a new set of global tariffs, first 10%, then ratcheting up to 15%, using a different legal mechanism that allows trade restrictions for up to 150 days. There is already speculation that the administration will seek ways to extend these measures beyond the initial period.

This piecemeal and arbitrary approach to tariffs is a headache for businesses and consumers alike as they are left guessing about what the future might hold. The government itself faces a conundrum as any future roll-back of tariffs (whether due to legal challenges or eventual policy shifts) would shrink the revenue it’s counting on to fund priorities like increased military and border spending, not to mention recently promised tax cuts. The Court’s ruling has also prompted talk about whether US companies might attempt to reclaim some of the tariffs they’ve already paid over the past couple of years. In theory the sums at stake are enormous, potentially hundreds of billions of dollars, but there’s no clear process for how, or even if, such refunds would occur, and most observers doubt consumers would see any direct relief from the higher prices passed on since the trade war began.

It’s worth noting that despite the political drama, the economic impact of the now-prohibited tariffs was not as profound as advertised. Trump has claimed the trade war slashed the US trade deficit by 78%, but the actual data for 2025 show the deficit was a mere 0.2% smaller than the year prior. And if the tariffs were intended to hurt China, they largely missed the mark: China’s exports to the US did fall, but exports to other countries more than compensated, leaving China’s overall trade position relatively unscathed.

So far in 2026 we’ve already seen a number of themes competing for headlines and driving returns and our focus on diversification and valuations has proved beneficial. We continue to believe in the transformative potential of technology (AI very much included), but we also know that even the most exciting growth stories must eventually be grounded in economic reality.

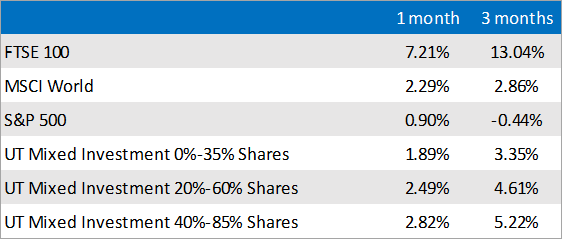

Market and sector summary to the end of February 2026

Source: Financial Express Analytics.

Past performance is not a guide to future performance, nor a reliable indicator of future results or performance.